You may recall that in "Super Size Me," documentarian Morgan Spurlock explored the effects of consuming a diet consisting solely of fast food from McDonald's. He decided to eat only McDonald's food three times a day for 30 days while following certain rules like always accepting the option of "supersizing" his meals whenever offered. He documents the effects of this diet on his physical and mental health, as well as on his weight and general well-being.

The film received critical acclaim and sparked public discussions about the health impacts of fast food, leading to changes in the fast-food industry, such as the introduction of healthier menu options and the discontinuation of the "supersize" option in some fast-food chains.

Throughout the film, medical professionals monitored Spurlock's weight and blood health. At the start of the experiment, Spurlock weighed 185 pounds with a body mass index (BMI) of 23.2, which is considered healthy.

After just a few days of consuming only fast food, Spurlock began to experience negative health effects. He gained a significant amount of weight, and his BMI increased to 25.5, which is considered overweight. By the end of the experiment, he had gained 24.5 pounds, and his BMI increased to 30, or obese.

In addition to the weight gain, Spurlock's blood health also deteriorated over the course of the experiment. His cholesterol levels increased by 65 points, and his liver function tests showed signs of damage akin to that of an alcoholic. He experienced dramatic mood swings, headaches, and decreased energy levels. He would get flat-out hangry when he'd gone more than a few hours with his Mc-y-D fix, and then upon diving into a Big Mac, he'd be as mollified as a heroine junking staving off the demons.

But did Spurlock prove that all fast food is unhealthy, or did he highlight the deleterious effects of highly refined carbohydrates, the industrial byproduct of seed oils, and the chemical cocktail of preservatives?

One of the most intriguingly disturbing parts of the documentary was when Spurlock purchased an order of McDonald's fries and kept them in a container for 10 weeks to see how long they would last without molding or decomposing. He stored the fries in the container at room temperature and did not add any preservatives or chemicals to the fries. He also did not open the container or disturb the fries in any way. After 10 weeks, Spurlock checked the fries and found that they had not molded or decomposed whatsoever.

Well, I think we have our answers, as this chap loses weight, experiences no loss in athletic performance (rock climbing), and generally maintains similar blood health (with a remarkable improvement in triglycerides).

If you want to skip to the results, jump to the 45-minute mark and just watch for about 20 to 25 minutes. Petty staggering how well things turned out.

According to the Canadian Institute for Health Information (CIHI), the median wait time for priority procedures in Canada in 2020 was 16.8 weeks, up from 10.9 weeks in 2019. Priority procedures are defined as procedures that are clinically necessary, but their delay could result in the patient's condition becoming more serious.

However, wait times vary widely depending on the province or territory and the specific medical facility. In 2020, the median wait time for priority procedures ranged from 10.6 weeks in Quebec to 32.9 weeks in Prince Edward Island. Even the median wait time for cancer-related surgeries was 4.8 weeks.

Patients are often forced to travel to a different province to try and get care more quickly.

This is a summary of the current situation from the Mises Institute:

Currently, there are approximately 1.2 million Canadians stuck on a government waiting list for healthcare that they need. This is a death sentence for many of them, as it has been for thousands of patients who have gone before them. ...

Patients who endure considerable suffering as they languish on a waiting list—where many of them die—cannot be seen to have been given reasonable access to health services in the government’s Medicare system. The government also prevents them from having reasonable access to a private healthcare option.

Thus, reasonable access is an obvious deception, with benefits flowing to highly paid, power-hungry politicians, bureaucrats, and administrators wanting to maintain control over massive, inefficient healthcare bureaucracies at the federal and provincial levels. This deceitful behavior fits the definition of fraud and should be prosecuted as such.

Thousands of Canadians die while they wait for the care that the government promised to deliver when they needed it. ...

If politicians were personally accountable for the damage they caused, guess what? They wouldn’t cause any damage! However, we cannot hold them personally accountable because equality under the law does not exist in a democracy.

In the private sector, you are accountable for your own actions. If you break your neighbor’s window, you pay for the replacement. If you are a politician and you break the window in the course of performing your official duties, you can charge the cost of the new window to taxpayers....

When citizens demand better service, politicians respond by saying, “Okay, but that means we have to take more of your money.” So, taxes are raised, more bureaucrats and administrators are hired, and the inefficient Medicare bureaucracies that politicians and bureaucrats regard as their personal fiefdoms grow ever larger. That’s why healthcare is the single largest item in many provincial budgets. ...

AI is being used extensively in the area of the pre-authorization of your medical claims. Prior to approving a medical service or procedure, insurance companies often require a pre-authorization process where doctors must submit detailed information about the medical necessity of the service or procedure. AI algorithms can analyze this information to quickly determine whether the service or procedure meets the insurer's criteria for coverage.

Lawfully, AI is not supposed to autonomously make these decisions without human intervention. The final decision on whether to approve or deny a claim is supposed to rest with human reviewers who use the information provided by AI systems as one of many factors to consider. So what happens when those human reviewers are doctors that reflexively sign the denial in less than two seconds without reading or even opening the patient file?

Well, increased profits for the Government Healthcare Complex and a fresh glimpse at the utopia of AI medicine. This whole article is worth your time to read. It is an excellent glimpse behind the curtain. The following is from ProPublica:

The company [Cigna] has built a system that allows its doctors to instantly reject a claim on medical grounds without opening the patient file, leaving people with unexpected bills, according to corporate documents and interviews with former Cigna officials. Over a period of two months last year, Cigna doctors denied over 300,000 requests for payments using this method, spending an average of 1.2 seconds on each case, the documents show. The company has reported it covers or administers health care plans for 18 million people....

A Cigna algorithm flags mismatches between diagnoses and what the company considers acceptable tests and procedures for those ailments....

'We literally click and submit,' one former Cigna doctor said. 'It takes all of 10 seconds to do 50 at a time.'...

Cigna does not expect many appeals. In one corporate document, Cigna estimated that only 5% of people would appeal a denial resulting from a PXDX review.

"According to a new report from Care.com, many U.S. employers are looking to revamp their benefits packages this year. The survey suggests that 95% of leaders are planning to re-examine their strategies, with nearly half of respondents – some 47% – looking to cut back benefits. ...[W]hen leaders were asked about what benefits they planned to cut, top answers included adoption/fertility assistance, commuter benefits, education and wellness resources, health and fitness discounts, and home office stipends."

FSAs (Flexible Spending Accounts), HSAs (Health Savings Accounts), and HRAs (Health Reimbursement Arrangements) are all types of tax-advantaged accounts that can be used to pay for qualified medical expenses.

Physical therapy, nutritional supplements, and gym memberships may be eligible expenses that can, in rare cases, be reimbursed using these accounts, but there are some specific rules and limitations about which, you must be cognizant.

For FSAs, eligible expenses are determined by your employer's plan and may vary. You can usually use FSA funds to pay for physical therapy with a prescription from a healthcare provider. Nutritional supplements and gym memberships are likely not eligible expenses, unless they are prescribed by a healthcare provider for a specific medical condition.

For HSAs, physical therapy, nutritional supplements, and gym memberships may be eligible expenses, again, if they are deemed medically necessary by a healthcare provider. In that case, you can use HSA funds to pay for these expenses as long as they are not considered cosmetic or meant for general health and wellness purposes.

For HRAs, the rules and eligibility requirements will vary depending on your employer's plan. It's important to check with your employer or plan administrator to see if physical therapy, nutritional supplements, or gym memberships are eligible expenses. In most cases, these procedures will only be covered if they are deemed necessary by a healthcare provider.

In general, it's important to keep receipts and documentation of your expenses, and to check with your plan administrator to make sure that the expenses you are considering are eligible before using your FSA, HSA, or HRA funds to pay for them.

The IRS recently issued new guidance on this topic. There was nothing earth-shatteringly new in their statement, but more clarity has been provided. Here is a summary of the IRS's pronouncement by Thompson Reuters:

For the cost of therapy to be a medical expense, the therapy must treat a disease—thus, amounts paid for therapy to treat a diagnosed mental illness are medical expenses, while amounts paid for marital counseling are not. Likewise, the costs of nutritional counseling and weight-loss programs are medical expenses only if the counseling or program treats a specific disease diagnosed by a physician (e.g., obesity or diabetes); otherwise, these costs are not medical expenses. The cost of a gym membership is a medical expense only if the membership was purchased for the sole purpose of affecting a structure or function of the body (e.g., a prescribed plan for physical therapy to treat an injury) or treating a specific disease diagnosed by a physician (e.g., obesity or heart disease). However, the cost of exercise for the improvement of general health is not a medical expense, even if recommended by a doctor.

There are more self-funded than fully insured plans among companies with 100 or more employees (38,000 vs. 32,000). And if you are an employee at a company with 100 or more employees, you are twice as likely to be covered by a self-funded plan as a fully insured plan.

I'm a sucker for all of these types of lists. This one is from Wallet Hub. The map below is interactive, and you can hover over any state to see where it ranks. If you hit the Wallet Hub link you can review their methodology.

5 States with the lowest tax burden (best at bottom):

New Hampshire

Wyoming

Deleware

Tennessee

Alaska

5 states with the highest tax burden (worst at top):

Remember that “rule” in Obamacare that required all your preventive care and annual health exams be "free?" It was a blissful notion conjuring up unicorns flying across the sky, sprinkling fairy dust from their rainbow-colored stethoscopes.

We told employers and employees then - don’t count on it. First of all, nothing is ever free. The new law simply meant that all the preventive care you were supposed to get in a given year, would now be pre-paid with higher premiums. In other words, if you did not go to the doctor each year and maximize all of the preventive care that would be appropriate for someone of your health, age, and sex, you’d now be overpaying as all of our premiums increased by about 1 percent to cover the government mandated pre-payment racket.

So, how is this manifesting as double payment for many folks?

All our premiums went up 1% to prepay for it; and

If you aren't a hyper-diligent health-bill-nazi, you're likely being double-billed now when your doctor’s office keys in that you had a preventive exam as well as discussion, follow-up on, or evaluation of X. Where “X” can be any ailment, bump, sore, cut, tick, twitch, stressor, or annoyance in your life.

Our medical system even has a procedural code for “bitten by duck, initial encounter.” It is W61.61XAICD-10, in case you’d like your physician’s office to use it on your next visit. Please, if you do, don’t confuse that code with being “struck by a duck.” That is code W61.62. There are 155,000 codes in the ICD-10 system, in case you were wondering. And yes, because I know it is burning in the back of your mind as you read my scintillating post, there are codes for subsequent encounters with ducks as well; and for mere “contact” with a duck. U.S. Healthcare has ducks covered. But Cornish game hens? Not so much. In that case, you’d have to go with “pecked by chicken,” under ICD-10 code W61.33.

To say that our system has been bureaucratized beyond recognition into some sort of Frankenstein monster of public-private plunder is an understatement.

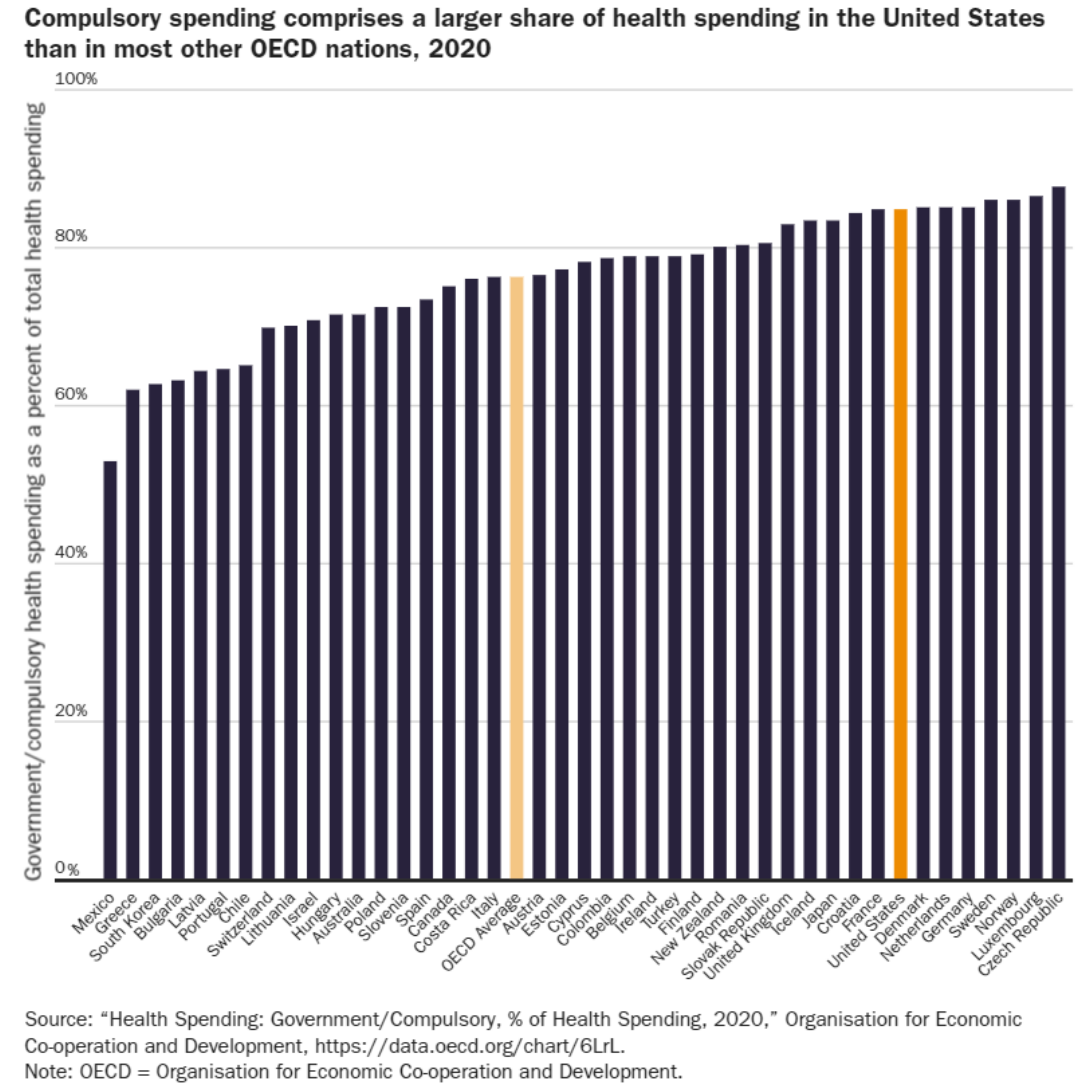

The government controls a larger share of health spending in the United States (85%) than in 30 other advanced nations, including Canada (75%) and the United Kingdom (83%), each of which has explicitly socialized health systems.Source.

So, are preventive visits pre-paid and copay-free under Obamacare? Only if you have impeccable health and you and your doctor do not discuss your blood pressure, blood glucose levels, sun exposure, moles, sniffles, or whether you’ve been pecked by a Cornish game hen. Of course, some doctors get it and are more forgiving than others. There are cases where you can get away with your depraved, thieving ways and attempt to get free healthcare advice during your purely preventive visit by asking about that odd little bump that’s appeared in your nether regions. Bandit!

Real-world advice: if your doctor asks you if there is anything else bothering you in your physical, and it is something minor about which you were mildly curious, say, “yes, I do have another question, but it is kind of a silly one and I don’t want to be billed for moving our visit beyond a purely preventive visit.”

A good doctor will gladly answer your question and not bill you. If your doctor doesn’t roll that way, it’s a decent sign that you may need a new doctor.

Now, if the issue is large enough that you want to discuss it and don’t care if it goes on for a few minutes, then by all means, ask. But know that your free exam just moved into an office visit for which you will pay a copay, co-insurance, or the visit cost if you are on a high-deductible health plan. But what would you rather do, finish this visit for free and then return in a few weeks to address the burning topic? If you do that, you’re doubling your time and will still pay for the visit.

Here is how Yahoo News covered this new phenomenon that’s been around for more than a decade (highlights are mine):

‘I got scammed’: Americans describe getting surprise medical bills via health care loopholes

Sometimes a simple coding mishap can result in a major headache for a patient, as was the case for Anthony, a 29-year-old based out of Norwalk, Conn.

When Anthony visited his doctor for a routine annual checkup — which his insurance plan through Cigna advertised as 100% covered without a copay — he ended up receiving a bill for $132.09.

This was because his doctor’s office coded the visit as an “office visit” instead of an “annual checkup or preventative care.” In an effort to clear up the confusion, Anthony called both Cigna and his doctor’s office, and Cigna assured him that it was simply listed under the wrong code and would be covered if the doctor’s billing department corrected it.

“I submitted a complaint to Westmed, and they forwarded it to the billing department,” Anthony told Yahoo Finance. “They rejected my request several times. According to them, the office staff had the final word on the billing code. I was able to talk to the office staff directly too, but I’m not sure who was responsible for selecting the billing code there.” …

“Wasted a bunch of time, and, frankly, I got scammed," Anthony said. "In the end, I got no explanation why they used the wrong code, and the bill was sent to collections. It’s going to hurt my credit score and in the U.S., that also means my ability to find a place to rent or even buy a house if I ever get the chance. It’s the kind of thing you lose sleep over.”

'They think short-term'

A loophole in the ACA — commonly known as Obamacare — is part of the reason why this issue persists in the U.S.

Under the ACA, insurers are required to cover preventive services such as cancer screenings, immunizations, and well-woman visits without cost-sharing, meaning that the individual receiving the services is not required to pay anything.

A study published in 2021 in the journal Preventive Medicine found that “in addition to premium costs meant to cover preventive care, Americans with employer-sponsored insurance were still charged between $75 million and $219 million in total for services that ought to be free to them.” …

Not-so-free procedures

Because of these loopholes, patients often find themselves billed for routine procedures that typically are fully covered by their health insurance.

Several individuals, who asked to remain unnamed due to privacy concerns, shared with Yahoo Finance the forms they were required to sign in order to be seen for routine physicals and other preventive exams.

In one of the forms, an individual was told that if they discussed any new or chronic medical issues with their doctor, their insurance would be billed for both an office visit and a preventive health exam.

For another individual, their form indicated that if they discussed new acute conditions or a worsening chronic condition, if a diagnostic test was ordered, or if a treatment changed, they would also be subject to two separate bills.

“There are a lot of gray areas but generally, those shouldn’t be billed,” Jenifer Bosco, a staff attorney at the National Consumer Law Center, told Yahoo Finance. “In the worst case, some providers do engage in what’s referred to as upcoding where they will try to bill for things or get reimbursed at a high rate for things that really should be either preventive or should be billed at a lower rate.”

For example, a preventive colonoscopy meant to screen for cancer is required to be covered at 100% by health insurance providers. However, if a polyp is discovered and removed from the patient during that screening, that procedure becomes a “surgery” rather than a screening and is billed as such.

“It makes zero sense charging the cost of something or the cost to the patient for something while they’re literally mid-procedure,” Bosco said. “You can essentially bill two visits for the same time, which I think intuitively just doesn’t make a lot of sense to most people. If you’re going in for one visit, how can you be charged for two and also be losing that free preventive visit at the same time?”

According to the Preventive Medicine study, patients were saddled with a total of $12.8 million for preventive colorectal screenings in 2018, while wellness visits incurred charges of up to $73.1 million.

“It feels a little bit like a bait and switch, and that’s not on the doctors,” Shafer said. “That’s just how we’ve set up the reimbursement guidelines and everything else. It’s frustrating.”

The Compliance Traps, Administrative Nightmares, Subtle Discrediting & Employee Frustration Voluntary Benefits Often Bring

Special guest column by Dagny

Taggart | March 2023

As a wee lass, my grandmother used to admonish, “don’t go

borrowing trouble.”

I only fully internalized or “grokked,” as the kids say,

that message once installing voluntary benefit plans.

In the eyes of the ginormous corporations that have devoured

nearly all the insurance brokerage market, I’m reasonably sure this makes me a

bad broker. Because, you see, once you are publicly traded, your stock prices

and your national VP’s job are tied inextricably to the holy grail of

growth. Client retention is nice and may

even earn you a pat on the head or some other form of little doggie treat, but growth,

my lass, well, that shall set ye free!

I’ll never forget a conversation with a notoriously

unscrupulous brokerage owner in the San Francisco Bay Area. We were at some

stuffy, pompous, self-congratulatory industry meeting where brokers take a

temporary leave from the golf course to discuss how to best grow revenue (your

premium).

The greasy, slick-haired, dark pinstripe-suited,

mafioso-looking founder told our CEO, “I’ll never understand why you put so

much stock in retention. Once a client has identified that you cannot service

them as promised, it will still take them nine to eighteen months to leave for

a new broker. You can sell a handful more groups in that time!”

Even though that was nearly 25 years ago, very early in my

career, I always remembered the message.

And I hated it increasingly each year I practiced.

As a brokerage office is purchased by a bank, merged with

another bank, and repacked to a private equity firm like every other financialized

product in our country, brokers are inevitably hounded with the mantra of

growth. New sales conquest lists are circulated monthly, sometimes weekly, to

prod already organically competitive salespeople to climb over each other to

push more premium dollars through their P&Ls. One company I worked with

even created a gameshow-like point system to maximize salesy behavior.

Referrals to decision-makers, cold calls made, meetings attended, and spam sent

all earned various forms of atta-boys from the official brass. Meanwhile, 20-plus-year

veterans who consistently renewed multi-million-dollar books of stable clients

were regarded as an annoying relic to a bygone era in American Business: a time

when steady service, professionalism, and integrity hindered the mantra of G-R-O-W-T-H.

Enter Voluntary Benefits

Voluntary benefits offer a quick fix for a stagnant book of

steady, satisfied clients. It is the cocaine bump from the countertop in the club

bathroom when a partier doesn’t have the energy or personality to peacock with

the amplified type-As. With voluntary benefits, an employer can roll out

additional life, disability, accident, cancer, critical illness, pet, home,

auto, gap, dental, vision, or hospital insurance at no cost to the employer and

only for those employees who want to purchase it. As the pitch goes, it rounds

out your offering, maximizes choice, and gives people more opportunity to cover

what is important to them. Who could be against that?

And I must admit, as a budding, libertarian-minded little

brokerita, I bought into the concept. Voluntary benefits were, after all, voluntary

and offered commission to the brokerage of an additional 15 percent to 55

percent, depending on the line of insurance offered. Employees win, the

employer wins, and the broker wins!

Alas, there is no free lunch. Imagine a product that is half

commission. How can an insurer afford to sell you something that is half

commission?

Hint: it is not by undercharging for the

product.

What’s the Real Message?

As much as every broker and I want them to be, your

employees are not benefit experts. Let’s be frank: your HR team probably isn’t

either – at least most aren’t. In fact, your employees hate dealing with

benefits, particularly the insurance side, so much that they spend an average

of eighteen

minutes making open enrollment decisions. By contrast, they will spend four

hours on the decision to buy a cell phone. Priorities.

No array of glossy brochures, automated video open

enrollment meetings, or highly entertaining broker personalities [ahem] will

drastically change that. A fantastic broker and presentation package might

get their attention for forty-five minutes. And I know because I regularly do

[smiling].

When we add V.D. (what I call voluntary dental) to your

plan, as an example, we will divert attention away from where eighty percent of

your benefits budget goes – toward medical. Why would we do that? Of course, if

all you offer is medical and V.D., that is not a problem. But most employers

offer employer-paid medical, life, dental, vision, employee assistance

programs, and disability. Communicating that to employees takes the entire

forty-five minutes. If we attempt to add the laundry list of other items from

earlier in the article, we confuse and frustrate your audience.

But what else are we effectively saying?

Our benefits are not good enough to cover you and your loved

ones should tragedy befall you or your family. Sure, we offer you a few

employer-sponsored items, but you probably need to buy all the other items this

pushy salesperson is here to deliver. There is a watering-down effect, and you

taint the vital quality plans like group disability and medical with the

lottery-esque nature of cancer or accident policies. It’s what my 20-year-old

daughter would call a “low-key dis.”

Pro Tip:Brokers don’t buy the

laundry list of benefits. Brokers buy medical, disability, and life if we have

dependents and are in a phase of life without enough assets to cover mortgages

and college tuition. Everything else is superfluous. One of the best things we

can do as insurance and human resources professionals is to help educate our

employees on the real need for insurance. Insurance is for the huge risks we

cannot plan for or save for: death, disability, and serious medical issues. We

can and should be able to save and plan for dental, vision, accidents, pet

issues, etc. If one can’t, then they just aren’t trying. If you set aside the

money you’d pay in premium toward your dental, vision, etc., you will have that

money when the need arises; and you will not have to hand over 15% to 50% in

commission and another 10% for carrier profit.

Administrative Hell

Much like third-party administrators and human resources

information systems, voluntary benefit providers systematically over-promise

and under-deliver. Here is a partial list of what every employer should expect when

installing new voluntary benefit plans:

The carrier will not enroll all of your

employees correctly. There will be some with misspelled names, incorrect dates

of birth, wrong benefit plans, and incorrect family tiers. Some may be dropped

from enrollment entirely for no good reason.

This will increase the HR department's workload

and hours will be spent on the transition. It will also cause disruptions to

the organization due to meetings, forms that need to be completed, and the inevitable

discontent from some employees.

If a company is going to add voluntaries, the

CEO or other high-ranking executive should announce the change - and the

business reason why - before the meetings.

Depending on the type of product you offer, you

may have to meet minimum participation levels. This means, for example, if 20%

of your employees don’t elect to buy additional life insurance, you will not be

able to offer it to any of them. And you may have just had 15% of them sign up.

Now you get to go back and tell those 15%, “nevermind.”

The first bill will not be accurate. The client must

audit the first bill immediately upon receiving it and notify the carrier of

changes. A binder check for the first month's premium is required with the

master group application and will be credited on the first or second billing

cycle. Therefore, your first few bills are not likely to be accurate.

And that list assumes you already boast a savvy and robust

HR team. If you have new or inexperienced folks on the team or if you

experience regular turnover in HR, these matters can grow unruly in a hurry.

One Midwestern company I worked with churned through three

different benefit managers in eighteen months. HR was responsible for sending

an evidence of insurability form to employees who applied for more than the

voluntary life’s $100,000 guaranteed issue amount. That crucial detail was lost

in the shuffle. So, tensions rose when the employer experienced the death of an

employee who thought he’d purchased $300,000 of life insurance, and the carrier

asked the employer where the evidence of insurability was. I’ll shortcut to the

answer: to make the deceased widow whole, the employer had to self-fund the

additional $200,000 in life benefits, and the Director of Human Resources lost

his job. A forgotten form from a benefit manager on a voluntary life plan ended

a career and cost this employer $200,000.

If you are reading this and unsure what an evidence of

insurability is, do not offer voluntary benefits. That risk is too significant

for you and your organization at this time. If you are going to provide

voluntary life or disability, make darn sure that your broker explains these

potential nightmares to you.

Compliance Nightmares

Beyond the previous chilling story, a whole other compliance

issue can arise with voluntaries. Suppose there happens to be a legal dispute

between one of your employees and your voluntary vendor. In that case, that

vendor will almost certainly argue that the plan is covered by Employee

Retirement Income Security Act (ERISA) and that the employee’s lawsuit should

be filed against the employer instead of the insurer. If the court agrees, the legal

burden shifts to the employer. And in case you were wondering, yes, this one

also gets HR folks fired. Courts regularly rule that a voluntary plan is an

ERISA plan, even if the employer never intended to sponsor the plan formally.

And if that happens, and the plaintiff’s attorney is worth

his salt, they’ll also file claims against the employer for all the ERISA

reporting, disclosure, and fiduciary requirements that weren’t followed. Two of those penalties would be:

$149 per day penalty for failing to provide Plan

Document and SPD; and

$2,097 per plan per day for failing to prepare

and file Form 5500.

Furthermore, the legal standard for what mandates that ERISA

covers a plan is not a bright-line test. It is akin to the federal employee vs.

independent contractor standard, if you are familiar with that. It is a “totality of circumstances” test that

requires the plan to:

be completely voluntary without any employer contributions;

not allow the employer to endorse or “take credit for” the plan;

not allow the employer to receive consideration for collecting and remitting premiums;

not use the employer’s name, or associate the voluntary plan with the employer-sponsored benefit plans;

not communicate the voluntary benefits at Open Enrollment with all of the employer-sponsored ERISA-covered plans;

not recommend the plan to employees;

never say ERISA applies;

not allow the use of the employer’s cafeteria plan; and

not assist employees with claims or disputes.

In some cases, judges ruled that employers endorsed plans

because they announced the programs in memos written on company stationery. I’m

reminded of the old Jeff Foxworthy routine, ya might be a redneck ERISA

if …

Failing any of the above bullets might make your plan an

ERISA plan, depending on the court’s assessment of the action's severity and/or

frequency. Of course, failing to abide

by more than one further tips the scale in the direction of ERISA.

Benefit attorneys who litigate these types of cases regularly

report that 80% to 90% of voluntary benefit plans are, in fact, ERISA plans

once litigation commences and the voluntary provider makes this reflexive

initial motion.

And With All of That, There Are Some Places for Them

With all that said, is there ever a time when voluntary

benefits are a good idea? Yes, they can be appropriate and even desirable in a handful

of circumstances.

Voluntary home and/or auto

insurance is often just a link to a carrier that employees can quote

themselves. It is done at any time of the year and regularly gets employees an

additional 5% to 10% off, in addition to any other discounts for which they may

qualify. Employers regularly can and do stay out of these offerings.

Pet Insurance. As

with home and auto, it is typically just a link to a vendor that can and will

offer your employee a modest discount because they work for you. Like with home

and auto, I’ve never seen a pet plan morph into an ERISA plan.

Voluntary Group Life and

Disability. These are often no-brainers. Notice that I said group

coverage here. I do not like the idea of individual, 1099’d, 100% commissioned

enrollers sitting across from your employees and asking them what momma and the

baby will do when they die. No, this is

the option to buy additional life and disability above and beyond the core

employer offering. We communicate it in a group setting, and then treat it like

an ERISA plan as it is linked to your underlying life and disability. But know,

all my caveats in this piece's “Administrative Hell” section apply. If you

don’t have a seasoned, stable, savvy HR staff, you may want to consider holding

off on these lines for a bit.

Union Demanded Plans.Other than what I’ve mentioned here, I’d pass on

the voluntary stuff. But I do know that there are times when a workforce

demands it. I have seen that from time to time in union environments. In that

case, partner with an exceptional broker to find a voluntary provider with a

long, stable track record. Believe it or not, I have encountered those in my

career. They aren’t totally fictitious unicorns but are exceedingly rare,

glorious beasts to behold in the wild.

Dagny Taggartis a retired and recovering broker and attorney who spends most of her days in a walled compound in Galt’s Gulch, Colorado, walking

her Labrador and watching the squirrels cavort. After a 30-year career in

benefits, she retired in her early 50s and now consults with large employers

and brokerages on healthcare, benefits, and ERISA.

Healthcare and processed food are the two largest industries/employers and lobbyists in the United States. Pharma alone spends five times what the oil industry spends on lobbying and three times more than any other industry. Congress, the FDA, USDA, CDC, HHS & CMS will not bite the hand that funds them. To be sure, from time to time, well-meaning government classers do question the status quo and make noises indicating that they might do the right thing. They are swiftly crushed.

In 2010-11, members of Congress questioned whether U.S. taxpayers should be paying for Diabetes Water (soda) for Americans on food stamps (officially now called SNAP, Supplemental Nutrition Assistance Program). Note the word NUTRITION.

The Ten Companies Controlling Nearly All We Buy in a Grocery Store

Fifteen percent of Americans rely on SNAP for their “food.” Seventy percent of SNAP dollars are spent on highly processed garbage (essentially, what you find in the middle aisles of your grocery store – stuff that didn’t exist pre-1900). The number one SNAP expenditure? You guessed it – Diabetes Water! How did the company whose product was formerly spiked with cocaine decide to handle the matter? Why with more lobbying, of course!

They deployed their billions to call African American and Hispanic interest groups. They noted that the Diabetes Water Industry would like to share some of its resources with those interest groups, assuming said interest group wanted to support “low-cost calories and choice for its members.” The other implication floated was that Congress’ contemplation of eliminating soda from SNAP smacked of racism. Of course it did.

But they weren’t done there. Big Diabetes lobbyists then reach out to right-leaning legislators and interest groups to point out that the Big Government Nannyists were at it again, wanting now to micromanage what people could drink right here in the formerly free, good-ole, U. S. of A!

The result? Yeah, you know. Soda (or do you say pop, ya heartlander) remains the top food product purchased with taxpayer-funded nutritional subsidies.

And this is just about food stamps. Meanwhile, school lunches have regulatory controls that limit the amount of saturated fat those meals can contain. Cattle ranchers and pig farmers clearly aren’t doing their fair share to buy a legislator. Sugar’s upper meal limit? Infinity.

Need more evidence? This is the latest taxpayer-funded food pyramid advice, indoctrinating that Frosted Mini-Wheats and Lucky Charms are healthier than beef or eggs.

This is a crime against humanity. Do I care if people want to guzzle Diabetes Water or gobble Diabetes Kibble? No! The state should not be involved in any of this. But to the extent that it is and to the extent that I’m forced to pay for others’ “nutrition,” that advice and food should not poison them.

For more on this story, check out this interview with insider-turned-whistleblower @calleymeans and @KenDBerryMD. He gets right to the juiciest nuggets toward the very beginning of the video. Diabetes Water hired Calley to cultivate a list of civil rights organizations and African American pastors to fan the flames of racism whenever Congress stepped out of lined and threatened to curtail taxpayer funding of weaponized corn syrup.

I thought this piece from J. Sanilac was superb on the topic. I particularly dug his list of twenty "techniques that can help us to navigate the chaotic sea of character and find the truth."

Stop pretending ad hominem judgments are irrational and avoidable. Instead, accept that they're necessary and use them consciously and intelligently. As I explained in Part I, even the smartest and best informed person needs to rely on ad hominem judgments for much of his knowledge. If you pretend you can know everything directly, or even that you can suspend judgment for any question you haven't answered directly, you'll only sink yourself deeper into delusion, and your beliefs will be less rather than more accurate.

Don't delude yourself into assuming your own claims will be evaluated entirely on their merits. Instead, accept that you too will be the object of ad hominem judgments, and these judgments will significantly impact the reception of your claims. To be an effective knowledge disseminator you should signal trustworthiness with your track record, your outward presentation, your credentials, your character, and your alliances. Even if he has a brilliant idea, a man with no credentials, no connections, shabby clothes, and poor interpersonal skills will lose far more time lobbying to get that brilliant idea taken seriously than he would have spent if he'd polished his signaling first. Businessmen and politicians understand this intuitively. Unfortunately the kinds of men who invent important new ideas usually do not, perhaps because it's precisely indifference to signaling and partisanship that enables them to discover what other people overlook.

Use the black box method to test claims whose details you can't understand or evaluate directly. Just check the final outputs: if they're good, the information within the box is probably good too; if they're bad, the information within the box is flawed at best, and likely wrong.

Evaluate your sources' record. Do they have a history of making accurate predictions or producing good practical results? Those who've been right in the past are likely to be right again. And you too should try to build a track record of reliability, because in the course of time it will add weight to your claims. However, there's an important caveat, which I'll explain below.

Distrust prestige transfer. Some public figures try to leverage their record of success in one domain to create the impression of reliability in another, unrelated domain. For instance, someone who's distinguished himself as a linguist or chess player might try to transfer the prestige he's accrued in his original field to a new field, like political theory, where it hasn't been honestly earned. But success in different domains requires a different cognitive style, different strengths, a different knowledge base, and years of different experience. It's not uncommon for successful CEOs to have naive views about topics that don't directly impact their business operations. You can't assume the composers of masses are experts in theology, nor vice versa. So prestige transfer should awaken your distrust.

Evaluate your sources' incentives and disincentives. Sources who are incentivized for telling the truth are inherently more reliable. Yet when it comes to topics of public relevance, they rarely exist, and the best one can hope for is to find sources who aren't too highly incentivized for lying. Of course, a few rare people do compulsively seek and tell the truth due to an innate altruistic instinct, but they usually lack the motivation to explore complex topics in depth, and are therefore less useful than one would wish. (As previously mentioned, betting markets are an attempt at solving this problem.)

Evaluate your sources' cognitive styles and use this information to interpret their claims. Some people tend to be paranoid and overstate possible negative outcomes, others are indisciplined and jump on new ideas without thoroughly examining them, others are especially prone to partisanship, others are stubborn and never back down when they're wrong, etc. By identifying the character of a speaker you can estimate the risk he'll make a habitual error or exaggeration, and use this to translate his claims into a more accurate form. For instance, a paranoid thinker can be expected to overestimate risk, treating low probability futures as if they're matters of pressing concern, so when absorbing his warnings (e.g. about asteroids) you should downgrade their urgency.

Build a stable of trusted sources. Because past record is a good indicator of present reliability, it's important to observe your sources over a period of years. This is a time-consuming process by nature, so when you discover a reliable source you should consider him a valuable long-term acquisition.

Lower your confidence in the most popular sources. Sources and claims that are afflicted by higher than average epistemic load are amplified, especially in the social media ecosystem. Because of this the most prominent people are not the most reliable people. You should interpret great popularity among the general public as a negative sign with respect to trustworthiness.

Give obscure outsiders a chance. If you always follow the obvious signals of trustworthiness, like credentials, respectable presentation, and uniformly palatable opinions, you'll sometimes trap yourself in a cul de sac of mutually reinforcing conformists who've shut out dissenters. Once in a while you should make a foray into the wilderness, because obscure and disagreeable outsiders who are ridiculed, denounced, ostracized, and shamed by the mainstream occasionally are right when everyone respectable is wrong. Usually, of course, they're a waste of your time.

Estimate the effect of signaling load and attempt to correct for it. Comb through all your beliefs to determine which function as positive social signals, and lower your confidence in these beliefs. You should lower your confidence even more if you've fallen into the habit of using them as signals yourself. Of course, they might be true; but the expected pattern is for them to be exaggerated in the direction of optimal signaling, and they could even be empty fabrications. You should also raise your confidence in beliefs that send negative signals. It's likely that some of these are correct, but socially unpalatable, and therefore unfairly denounced. Of course, it goes without saying that you should try to avoid overcorrecting. (Note that a dissident subculture isn't immune to signaling load, but rather develops its own local signals that aren't functionally different from those of society at large. Thus, being a dissident, or contrarian, or minority does not in any way exempt you from the need to correct for signaling load.)

Estimate the effect of partisan load and attempt to correct for it. Most people already assume the truth falls somewhere between the extreme statements of opposing factions, so it might seem that correcting for partisan load is as simple as embracing moderation and aiming toward the center. However, this type of lazy centrism isn't actually a good way to find the truth. Political actors are experts at manipulating it. For instance, as we discussed earlier, they can use propaganda to portray their favored views as normal and centrist even if they're partisan minority views in reality. They can also can encourage their extremists to be more extreme in order to move the perceived center closer to their side. (E.g. Trust Network A says the answer is 1, Trust Network B says the answer is -1, a lazy centrist concludes the answer is 0. Whence political operators in Trust Network A can use a common sales tactic to get their way: by overshooting and claiming the answer is 3, they cause lazy centrists to conclude that it's 1, their original desideratum. Because they're vulnerable to this tactic, lazy centrists can actually encourage extremism!) There are, furthermore, plenty of historically verifiable cases where one side turned out to be wholly correct and the other wholly wrong, so that centrism would not have arrived at the truth. Thus, when you try to correct for partisan load, you shouldn't just take a moderate position between two sides and stop there. It's better to analyze the effects of partisan load carefully first.

Don't assume that partisanship as such is bad. Partisan load does degrade the accuracy of our beliefs, but that doesn't necessarily mean you should reject partisanship. The reason partisanship isn't wholly bad, and indeed the reason it's a natural instinct in the first place, is that it's entirely possible—even likely—that an enemy is really your enemy. In other words, one trust network may be a real antagonist whose members really wish to deceive you and do you harm because they have interests that are contrary to yours. Humans are individuals who exhibit tribal coherence. If you insist on being naive and judge everyone only as an individual, you and your allies risk defeat, and in the worst case, even annihilation. Someone who encourages you to ignore partisanship when a genuine conflict is underway is not your friend, but your enemy, or at best a fool. Before rejecting partisanship you should evaluate the whole landscape in detail and choose a side if need be.

Hide or camouflage unpopular views and signals of partisan alignment when trying to communicate to moderates, opponents, and general audiences. If you send the wrong signals or create the wrong associations you'll trigger an immediate rejection of your claims, no matter how good or true they are, because you'll be identified as an enemy and therefore dismissed. One solution to this is to focus narrowly on your issue of interest and avoid addressing other topics entirely. This prevents any controversial or partisan-aligned views you may hold from becoming a divisive distraction and reducing your impact. Another tactic is to advocate for positions that are more moderate than your actual beliefs, pushing for a direction and then pushing again rather than selling your ultimate target up front. Both of these approaches are in common use.

Use your instincts. We have fine intuitions for making ad hominem judgments in context, and the rational judgments we make in the abstract are quite myopic in comparison. Good instincts are a serious asset, so if you have them you should value them. This is not, of course, to say that they can never be wrong.

Use sensory information. Factual information is conveyed most efficiently in text form. However, information about the human subjects who transfer this factual information is conveyed most efficiently in audiovisual form, and some of the information that can be found in appearance and voice is completely absent from text.

Look out for hackers. Look for signs that someone is intentionally manipulating ad hominem signals to induce trust or distrust where they aren't merited. Unfortunately it's not always possible to identify bad actors before they've done harm.

Be forgiving of humans who are in the grip of bad ideas. I'm not so keen on this one myself, dear readers, but I feel at least obliged to mention it in order to signal care. All of us have some wrong and indeed outright stupid ideas we can't recognize as such. This isn't necessarily because we're stupid ourselves, although often that is indeed the case. Rather it's because ad hominem judgments, while unavoidable, are an imperfect source of knowledge, and they can't be relied on to filter out every bad idea percolating through our trust networks. We ought to be forgiving of others who are also in the grip of foolish ideas thus acquired, especially when they're young and inexperienced.

Avoid overconfidence. It feels good to be confident in the beliefs of your trust network. But for the reasons just mentioned, it's inevitable that this confidence will sometimes be misplaced. If you want to form a probabilistically accurate picture of the world you should abstain from the joy of overconfidence, and always remain open to the possibility that some of your beliefs are false. In fact, it's safe to assume that some of your beliefs are false.

Read fiction. As a writer, of course I would tell you to read fiction. So obviously you shouldn't trust me. But the reason I've littered this essay with so many examples is that, outside of real-world experience, narratives are the best means we have for thinking about and understanding ad hominem judgments and trust networks. Trust is the stuff novels are made of. Even cheap soap operas often take trustworthiness and trust networks as their main topic, with the drama unfolding around questions like: who's conspiring with whom, who's really on whose side, who's lying and who's telling the truth? If you keep your nose buried in numbers and make the mistake of dismissing everything else as wordy nonsense, you might end up trusting the wrong people and pay the price for it.